I have long advocated that financial and economic education should begin earlier and occupy a greater share of most children’s education than it does in most places today. The show “Are you smarter than a 5th grader” has gained popularity by reminding many of us how much we may have forgotten from our school days in subjects like geometry, grammar, or geology, but also shows the unfortunate truth that questions about debt, savings and investment are not taught about enough in schools, and this has been said before.

During the global financial crisis, financial products like CDOs and mortgage backed securities were blamed and called “complicated” by commentators, lawmakers, and even Michael Moore. Many of those articles or video clips were only a few pages or minutes long, which in many cases would be long enough to broadly explain how these instruments actually work. Even as an educated and experienced practitioner, I am quick to admit that over 99% of the world’s financial products (by volume) are structurally simple enough that they could be given to many 5th graders for extra credit math problems. Compared with chess, checkers, backgammon, or other games taught to 10 year olds that might take “10 minutes to learn, but a lifetime to master”, financial “games” have the advantage of being able to make far more winners than losers with simple understanding and proper use.

So here is a quick first take on a 5-minute introduction to structured finance that can be the foundation of so many different lessons in finance (even percentages are left in parenthesis as optional for students who haven’t covered them yet):

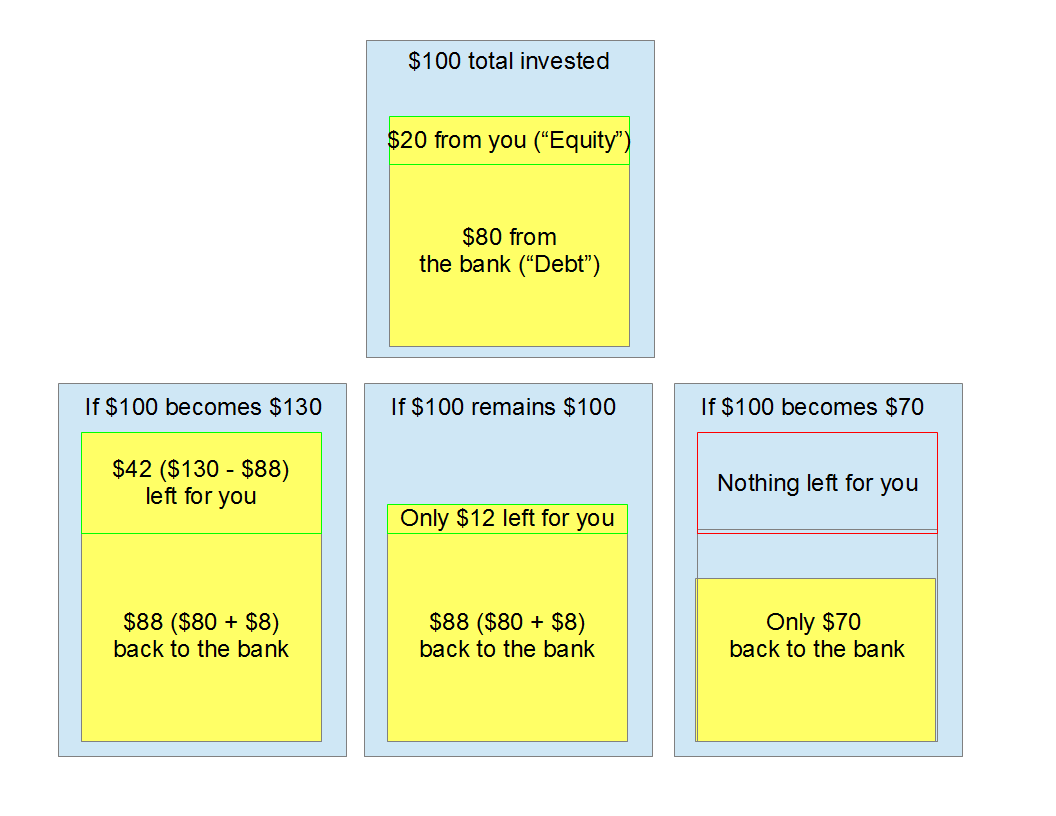

Say you have saved $20 and want to invest in a venture requiring $100 today. You expect this venture will turn the $100 into $130. This can be any money-making venture you can think of: a lemonade stand, equipment to paint a house, a trip to bring small tablet computers from China, etc.

Two different ways you can raise the other $80:

- You can find someone with $80 willing to share the profits and losses with you easily, the outcomes are easy to calculate: for every whole dollar of profit or loss, you get $0.20 and your partner the other $0.80.

- You find someone (say a bank) willing to lend your venture the $80 for a promised fixed return of $8 (10%) on their loan, meaning you need to pay them back a fixed amount of $88 when the venture is done. They have first priority on any returns from the venture, so you do not collect a penny until they have been paid their full $88, but beyond that all profits are yours to keep.

Now we explain what the return to you will be on your investment in three different scenarios: 1.) The $100 becomes $130 as you expect, 2.) the venture stalls, and the $100 remains $100, 3.) an unforseen loss occurs, and the $100 becomes only $70. As a diagram:

This of course is only one example of the building blocks that build the world of finance, but Richard Feynman once said about what many consider to be difficult physics: “We have come to the conclusion that what are usually called the advanced parts of quantum mechanics are, in fact, quite simple. The mathematics that is involved is particularly simple, involving algebraic operations and no differential equation or at most only very simple ones. The only problem is that we must jump the gap of no longer being able to describe the behavior in detail of particles in space.” Finance then has the advantage of not requiring such a cognitive jump, but rather the curiosity to ask and play, especially with play money, before expecting the next generation to perform all the roles in the global financial system that will soon be theirs.

This of course is only one example of the building blocks that build the world of finance, but Richard Feynman once said about what many consider to be difficult physics: “We have come to the conclusion that what are usually called the advanced parts of quantum mechanics are, in fact, quite simple. The mathematics that is involved is particularly simple, involving algebraic operations and no differential equation or at most only very simple ones. The only problem is that we must jump the gap of no longer being able to describe the behavior in detail of particles in space.” Finance then has the advantage of not requiring such a cognitive jump, but rather the curiosity to ask and play, especially with play money, before expecting the next generation to perform all the roles in the global financial system that will soon be theirs.

Another link on math skills expected of 5th graders: http://pumas.jpl.nasa.gov/examples/math_skills.php

2 thoughts on “Structured Finance for Fifth Graders”

I’m constantly amazed by how few people truly understand capital markets and how money is made. For political reasons it may be expedient to keep people in the dark, but this leads to repression. If more people knew how money is made it would lead to better, more informed policy-making. If more people knew how they could use these principles in their own life, wherever they fall on the economic spectrum, then they could get busy building the life they’ve always dreamed of.

You should definitely continue down this path, T. More posts, more graphics. Turn this into a book if you can.

Thank you K! I definitely would like to write a book explaining many important financial concepts at around the 5th grade level, and am still trying to make sure where the space is most underserved.

I don’t agree it is politically expedient to keep voters in the dark financially, and think it is one of those complicated issues where a historical legacy before financial literacy may take a few generations to work its way fully out of the system. I did like Thomas Jefferson’s answer to the idea of property qualifications for voting: instead of giving landless men the vote, it would be better to give them land (so that they would qualify to vote that way). By now most nations have universal sufferage, and there are probably more landless voters than ever, though hopefully many of them will build wealth in 21st century assets. A voting public that understands finance and how to manage it well is the best hope we have for a well-run, peaceful and prosperous world, so definitely time for our schools to step up to it!

Comments are closed.